All other things being equal, higher interest rates are a negative for real estate investment trusts or other businesses that rely on borrowed money to fuel growth. Rising interest rates tend to be a negative for all real estate assets in terms of valuation, so if interest rates remain higher, for longer, both construction and acquisition activities in the data center industry could slow, for a while.

Of course, rarely in life are all other things equal. Nobody believes demand for data center colocation, computing as a service or internet-fueled data storage demand is going to slacken. So any temporary slowdown in construction of facilities eventually produces shortages that drive higher demand for new facilities, a reinflation of asset values and higher interest in acquisitions.

To be sure, in the interim, higher interest rates will force firms to take a harder look both at construction and acquisition activities. But underlying demand eventually requires more construction, more capacity, more investment.

Private equity drove most of the 187 data center acquisitions in 2022, a level nearly matching the record level of 2021 activity. Higher interest rates are expected to crimp deal flow in 2023, though, since borrowed money finances private equity transactions, which have fueled the data center acquisition spree.

It might not be unreasonable to expect a dip in deal flow as the cost of borrowed money stays high. So acquisition multiples should contract a bit, deal flow should slow somewhat, deal size and volume could shrink.

On the other hand, underlying growth of demand for data center services should continue to grow at a strong clip, which will eventually combine with slower build patterns to reignite multiple expansion, making the assets more attractive again, even in the face of high interest rates.

Demand for data center assets has many drivers, attracting interest from growth capital, buyout, real estate, and infrastructure investors.

For growth investors, the attraction is higher expected revenue and above-average revenue growth rates. Buyout firms believe there are opportunities to create value by boosting the performance of underperforming assets.

For many the attraction is the perceived similarity of data center assets to other infrastructure assets purchased to diversify investment portfolios. Traditionally, those alternative investments have focused on real estate, airports, toll roads, seaports and energy utilities. Such assets provide a key perceived value: barriers to entry and predictable cash flow.

But digital infrastructure now is perceived as a new asset class with those desired characteristics. In addition to data centers, fiber-to-home assets now have joined mobile cell towers as assets in that category.

Of course, there are risks as well. Some believe valuation premiums might not be so warranted, longer term. The mix of demand from enterprise customers who shift from operating their own facilities to reliance on data centers could shift.

Though the shift to cloud computing generally has boosted demand for third-party data center capacity, scale often makes ownership more attractive than leasing. We see this in enterprise infrastructure quite frequently.

At low usage volumes, renting often makes much more sense than owning facilities. At high usage, the economics often reverse, and ownership becomes more affordable than leasing capacity. The mix of spending in a hybrid cloud or multi cloud environment could reverse, over time.

Hyperscalers who drive third party data center demand could slow their own demand for third-party assets or build their own facilities, which they have done in the past. On the other hand, the reverse should hold in expanding markets, where time-to-market considerations favor the hyperscale app providers leasing capacity from third parties, at least until volume kicks in and the economics of owning versus leasing change for them, as well.

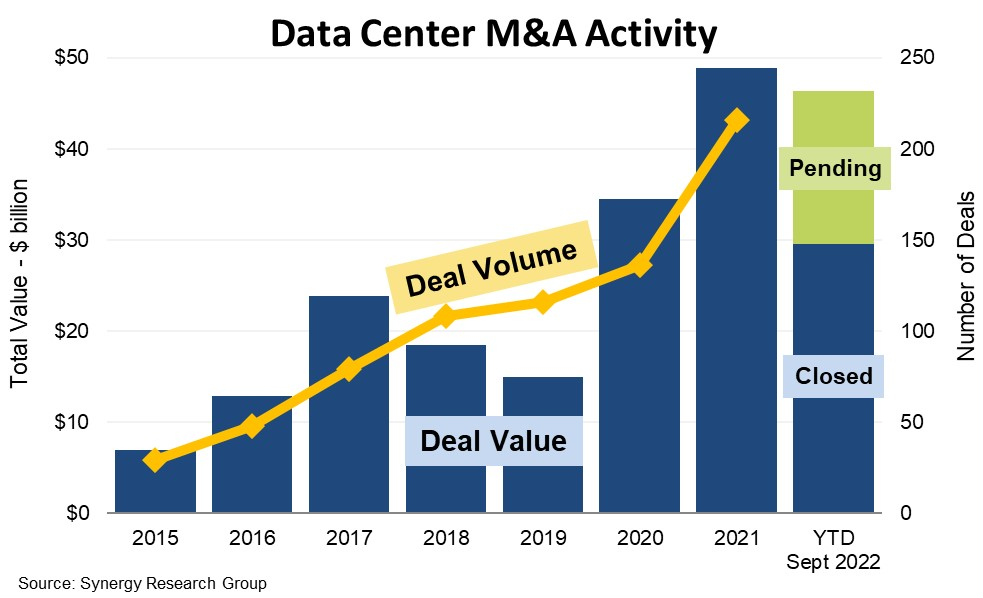

Deal volume has been growing since the mid 2010s. In the first nine months of 2022 there were about 150 data center mergers or acquisitions, says Synergy Research Group.

In 2021, there were 209 data center deals, with an aggregate value of more than $48 billion, up some 40 percent from 2020, when the deals were worth $34 billion, according to Synergy Research Group.

source: Synergy Research Group

In the first half of 2022, there were 87 deals, with an aggregate value of $24 billion.

From 2015 to 2018, private equity buyers accounted for 42 percent of the deal value. Their share increased to 65 percent from 2019 to 2021 and to more than 90 percent in the first half of 2022.

While interest rates remain elevated, organic growth will be quite important as a driver of data center asset valuation. In the near term, asset values should be compressed, at least a bit.

Of course, compressed valuations make those assets more attractive, since virtually everyone believes the long term need for data center capacity remains high. Lower interest rates will stimulate activity as well, but tighter supply will inevitably produce higher demand, even in the face of higher interest rates.

Time is part of the equation. As existing supply is soaked up, shortages will develop that must be remedied. And so investment will climb again. It is not a new story.

No comments:

Post a Comment