The edge computing market has many segments, including onboard device computing as well as premises and off-premises computing.

Looking only at consumer and enterprise devices that compute onboard, Deloitte suggests

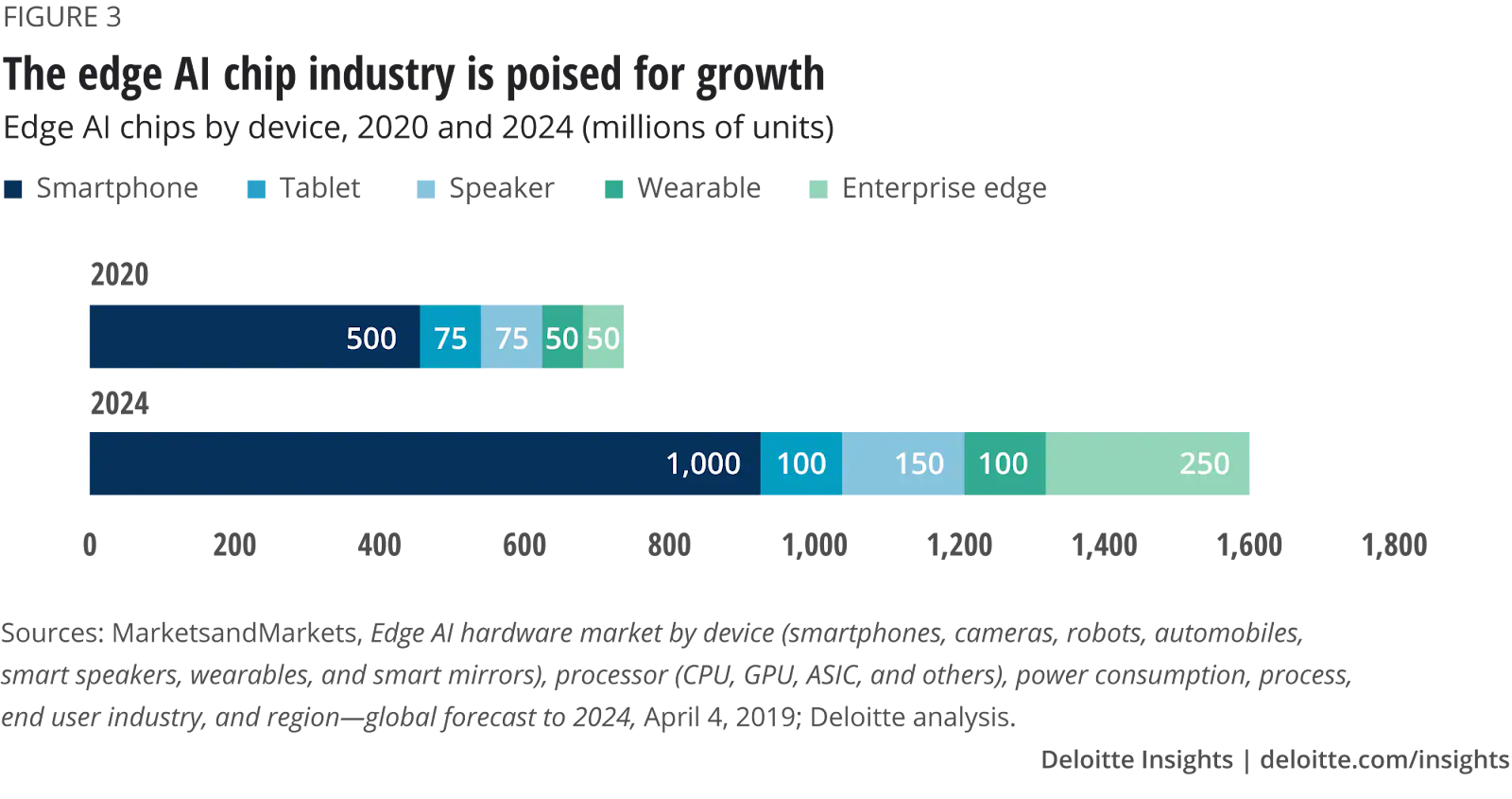

2020 sales of more than 750 million edge artificial intelligence chips that support machine learning tasks directly on the device, rather than in a remote data center.

Smartphones will be a huge part of the use case for AI chips at the edge, with other consumer devices such as wearables, smart speakers and tablets consuming 20 percent of those chipsets.

Not every segment of the edge computing ecosystem is directly concerned with AI chipset propagation, though. Mobile operators care about the relationship to mobile connectivity services, especially 5G, as well as opportunities to participate in premises or off-premises edge computing. Low power wide area networks also have opportunities for local access.

And many suppliers of local connectivity infrastructure also see key roles for premises wireless, including Wi-Fi and other short-range networks.

So virtually nobody believes that every internet of things use case “must” use 5G. That does not obviate the use case for 5G and ultra-low-latency connections, but there will be other connectivity options on the premises or for local access.

AI edge-related chipset sales might represent $2.6 billion in revenue, with a compound annual growth rate of 36 percent, says Deloitte.

“By 2024, we expect sales of edge AI chips to exceed 1.5 billion,” Deloitte sasy. That represents annual unit sales growth of at least 20 percent, more than double the longer-term forecast of nine percent CAGR for the overall semiconductor industry, according to Deloitte.

Analysts at ABI Research concur with at least parts of the Deloitte forecast. Revenue from cloud-edge artificial intelligence chipsets are set to grow from $2.6 billion in 2020 to $12 billion in 2025, at a compound annual growth rate (CAGR) of 36 percent, ABI Research predicts.

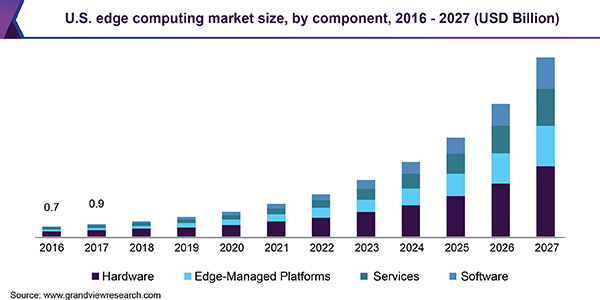

Many other forecasts might suggest similar growth rates for other parts of the ecosystem.. Grand View Research suggests 2027 edge computing revenues of perhaps $21 billion, going to suppliers in different parts of the ecosystem, ranging from chipsets to network infrastructure and software to services of many types.

If the Deloitte and ABI Research assumptions are correct, they suggest strong sales of smartphones and wearables.

The consumer edge AI chip market is much larger than the enterprise market, but it is likely to grow more slowly, with a CAGR of 18 percent expected between 2020 and 2024, say Deloitte analysts.

The enterprise edge AI chip market is growing much faster, with a predicted CAGR of 50 percent over the same time frame, Deloitte maintains.