Saturday, June 29, 2019

Suppliers Talk about Private LTE

A panel including Qualcomm, Cradlepoint, Ericsson, Athonet and moderator Sean Kinney discuss private networks based on 4G and 5G platforms. Speakers include:

Cameron McCaskill, Sr. Director of Business Development, IIoT - Qualcomm

Ken Hosac, VP of IoT Strategy & Business Development - Cradlepoint

Chris Wallace, Strategic Product Manager - Ericsson

Karim El Malki, President, Athonet USA & MulteFire member - MulteFire

Moderator: Sean Kinney, Editor in Chief, RCR Wireless News

Tuesday, June 25, 2019

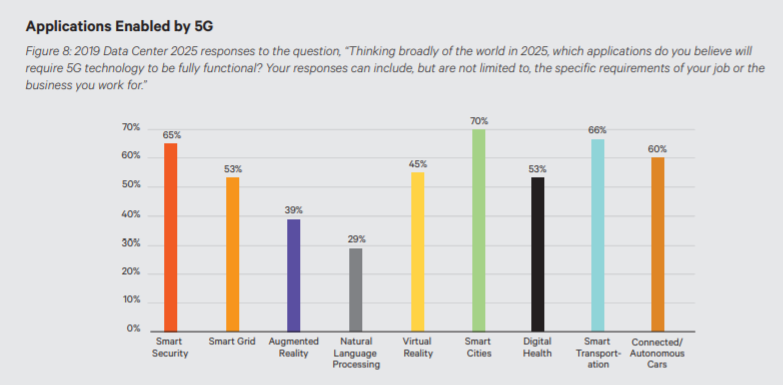

Data Center Execs Expect 5G Will be Quite Important for Many Edge Use Cases

Data center executives surveyed on behalf of Vertiv believe 5G will broadly support applications such as smart cities, smart transportation, security, connected vehicles, smart power grids and digital health.

Edge computing use cases come in four main buckets, according to Vertiv, which surveyed 800 global executives with data center roles.

Data intensive use cases where the amount of data makes it impractical to transfer over the network directly to the cloud, or from the cloud to the point-of-use, because of data volume, cost or bandwidth issues, make sense for edge computing.

This category includes smart factories, smart cities, high-definition content delivery and virtual reality.

Human latency sensitive use cases are a second category. Examples include augmented reality, smart retail and natural language processing.

Machine-to-machine latency sensitive use cases nclude arbitrage, smart security and smart grid.

Life critical use cases that directly impact human health and safety include autonomous vehicles and digital healthcare.

Of participants who have edge sites today or expect to have edge sites in 2025, more than half (53 percent) expect the number of edge sites they support to grow by at least 100 percent.

Some 20 percent of respondents expect a 400 percent or more increase in edge computing sites. For the 494 respondents already using edge computing, the total number of edge sites supported is expected to grow from 128,233 today to 418,803 in 2025—a 226 percent increase, Vertiv says.

Mobile Operrator Spending on Infrastructure Edge Capabilities Might Grow 53% Annually

Juniper Research forecasts that the total annual spend on mobile edge computing will reach $11.2 billion in 2024, up from $1.3 billion in 2019, a compound annual growth rate of 53 percent.

What is not clear is which parts of the market this revenue represents. It might be supplier goods used to create infrastructure computing capabilities. It might represent the fees enterprise customers pay connectivity providers to provide edge computing services. It might include both.

In this instance, it appears that Juniper Research is talking about hardware and software sold to service providers to create edge computing capabilities. The top five players are said to be

- Siemens

- Bosch

- AWS

- VMware

- Telit

That ranking suggests the market in question is infrastructure suppliers, and represents the value of hardware and software sold to service providers. The forecast does not appear to represent the revenue streams earned by connectivity and platform services providers selling edge computing to enterprise customers.

Monday, June 24, 2019

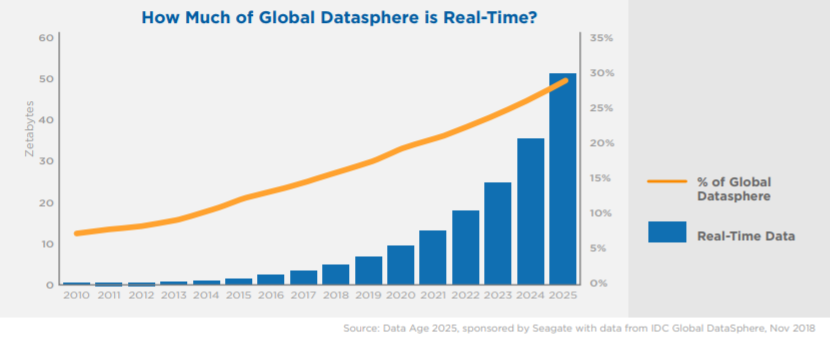

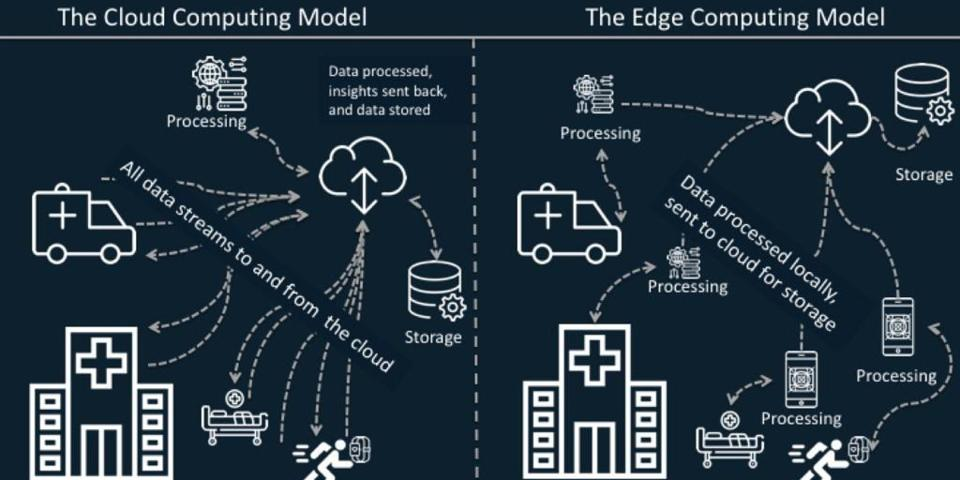

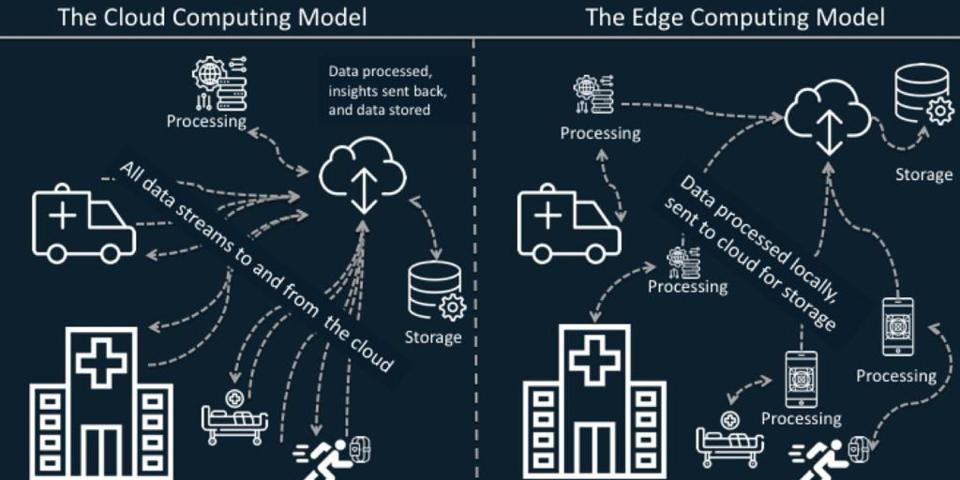

Big Shifts in Data Creation, Processing, Storage are Coming

While data storage is likely to remain “in the cloud,” processing is likely to move increasingly to the edge, driven by real-time apps and use cases, especially those related to internet of things apps.

This is a fairly good illustration of edge computing conducted by a device (personal health monitor, medical monitoring on the premises or at an edge data center. According to a study by International Data Corporation, 45 percent of all data created by IoT devices will be stored, processed, analyzed and acted upon close to or at the edge of a network by 2020.

{kind=link}

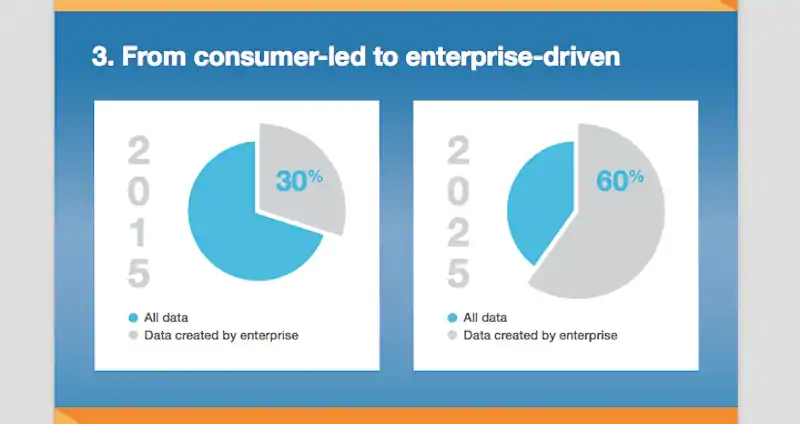

Some of us believe incremental new use cases and potential revenue in the 5G era will be driven mostly by enterprise use cases such as internet of things. The shift from consumer to enterprise for new revenue growth is mirrored by a huge shift of computing activity.

In the internet era, so far, data volumes have been lead by consumer apps such as streaming video, audio and web usage. By 2025, IDC predicts, volume will have shifted to enterprise. That, in turn, will

While data storage is likely to remain “in the cloud,” processing is likely to move increasingly to the edge, driven by real-time apps and use cases, especially those related to internet of things apps. In most cases, those IoT apps will be deployed by enterprises.

Friday, June 21, 2019

5G and Edge Computing are a Natural Fit

Nobody can yet be sure that connectivity providers will succeed commercially with their efforts to create a new role in edge computing as a service. But the advent of ultra-low-latency 5G networks, paired with computing and processing at the edge, represent a logical business opportunity.

Wednesday, June 19, 2019

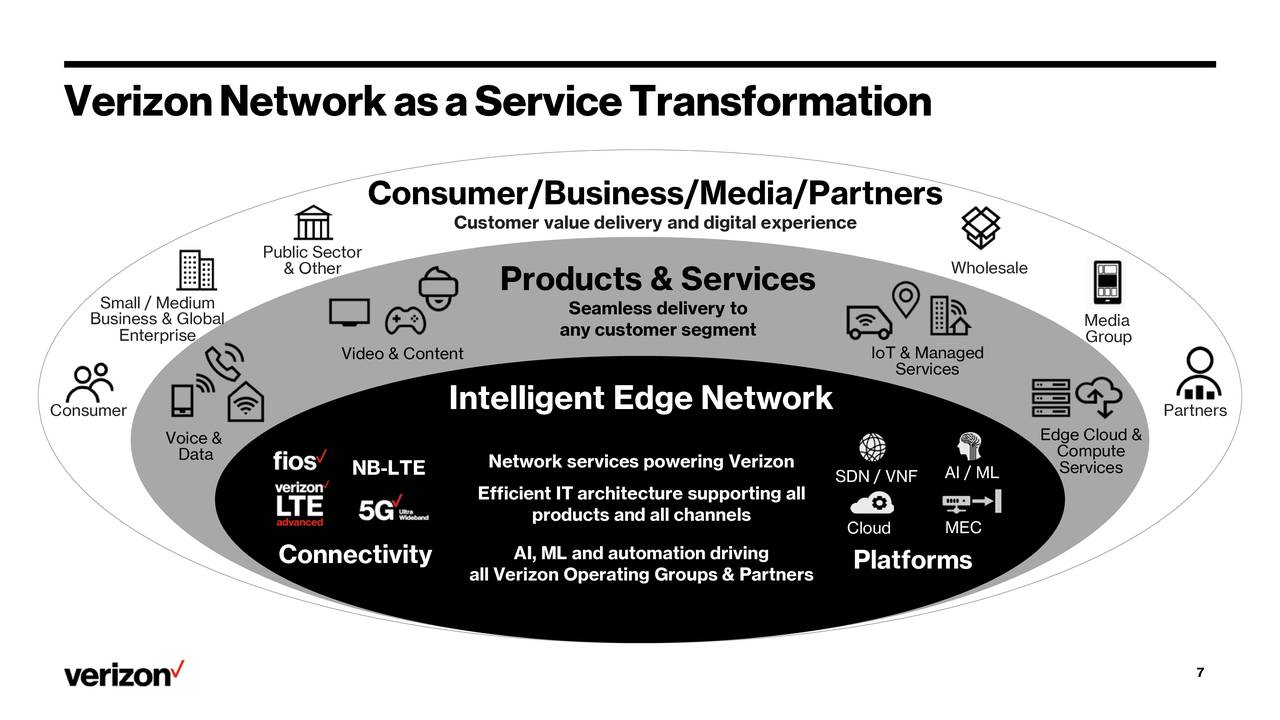

Verizon Sees All Revenue Streams Built on "Intelligent Edge"

Slideware, it often is noted, is not the same thing as operating results, available products and services. But it one noteworthy new Verizon slide illustrates at the very belief a vision for how Verizon wants to build its business.

Note that products and services, plus customer segments, all are supposed to build off an “intelligent edge network.” Of course, the edge itself includes core network platforms, but you get the point: intelligent edge is where Verizon sees its focus.

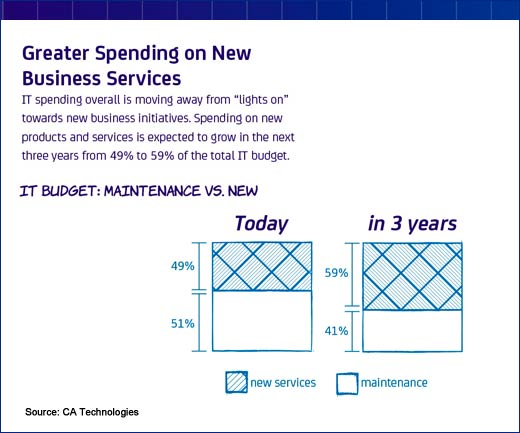

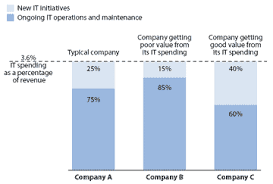

Will Enterprises Shift Spending from Maintenance to Digital Transformation?

No matter what our historical assumptions about enterprise information technology spending have been, they might be changing, away from on-going business processes and in the direction of digital initiatives.

The obvious question for many is what that means for aggregate levels of IT spending. It is reasonable to expect some growth, but it also is reasonable to expect that enterprises will shift some existing spending.

So one issue is ability and willingness to shift spending from maintenance to "digital" transformation.

By all accounts, the overwhelming bulk of spending is for maintaining or extending existing functions, not brand-new initiatives.

As a rule, IT budgets tend to stay relatively constant, while growth initiatives come out of that static bucket. So the issue is how much of the existing budget can be shifted to support internet of things initiatives.

How Big is Industrial IoT "Things" Market?

Internet of things is not an entirely-new development. Industrial and process automation spending already exists, using sensors, monitoring and control platforms and analytics that one day will be subsumed or augmented by IoT. But it is a good place to start.

In a broad sense, all existing industrial and process automation, monitoring, robotics might be counted in the existing “IoT” basket, even if the sensor systems do not actually use internet protocol, cloud computing or edge computing. But that creates a natural upper limit to the IoT market, if it describes all spending on systems that monitor processes.

A couple of obvious caveats are that such forecasts necessarily must include all enterprise spending for processes and systems that might eventually be considered part of IoT, including all process control systems, of any type.

So one fundamental assumption is that perhaps all existing forecasts are too optimistic, as some present spending will eventually be counted in the “IoT” basket. In that sense, some IoT spending will simply be a replacement for legacy spending, as much 5G subscription spending will simply replace existing 4G spending.

Over time, most control processes might switch to use of internet protocol for communications, digital sensors for collecting information and cloud, multi-cloud, edge or private data centers. In the interim, we might assume all estimates of IoT include the value of existing automation platforms, whether they are formally IoT or not, as replacement will almost-certainly move those expenditures into the IoT category.

Industrial sensors already are used in electrical power, natural gas utility, automotive and manufacturing settings, to measure pressure, current, temperature and flow, for example. By some accounts, $16 billion industrial sensors are sold every year.

Industrial wireless sensors might represent $3 billion to $4 billion in annual sales already. Optical sensors might generate $16 billion in annual sales, of which perhaps $3 billion to $4 billion already is used by robotics systems.

The global automation market, including factory automation, process automation, industrial software, 3D printing, artificial intelligence and drones is someplace between $150 billion and $200 billion globally, and already would include the value of sensor purchases.

Some estimate that hardware represents 20 percent of the cost of any initiative. Assume IoT hardware represents about 15 percent of all hardware used in an implementation. That implies IoT hardware could represent $23 billion to $30 billion in annual purchases.

Is IoT Part of Digtial Transformation Budget?

Is IoT in the broad category of digital transformation? Many would tend to say “yes.” If so, then IoT spending by enterprises might already be reported as part of such transformation initiatives.

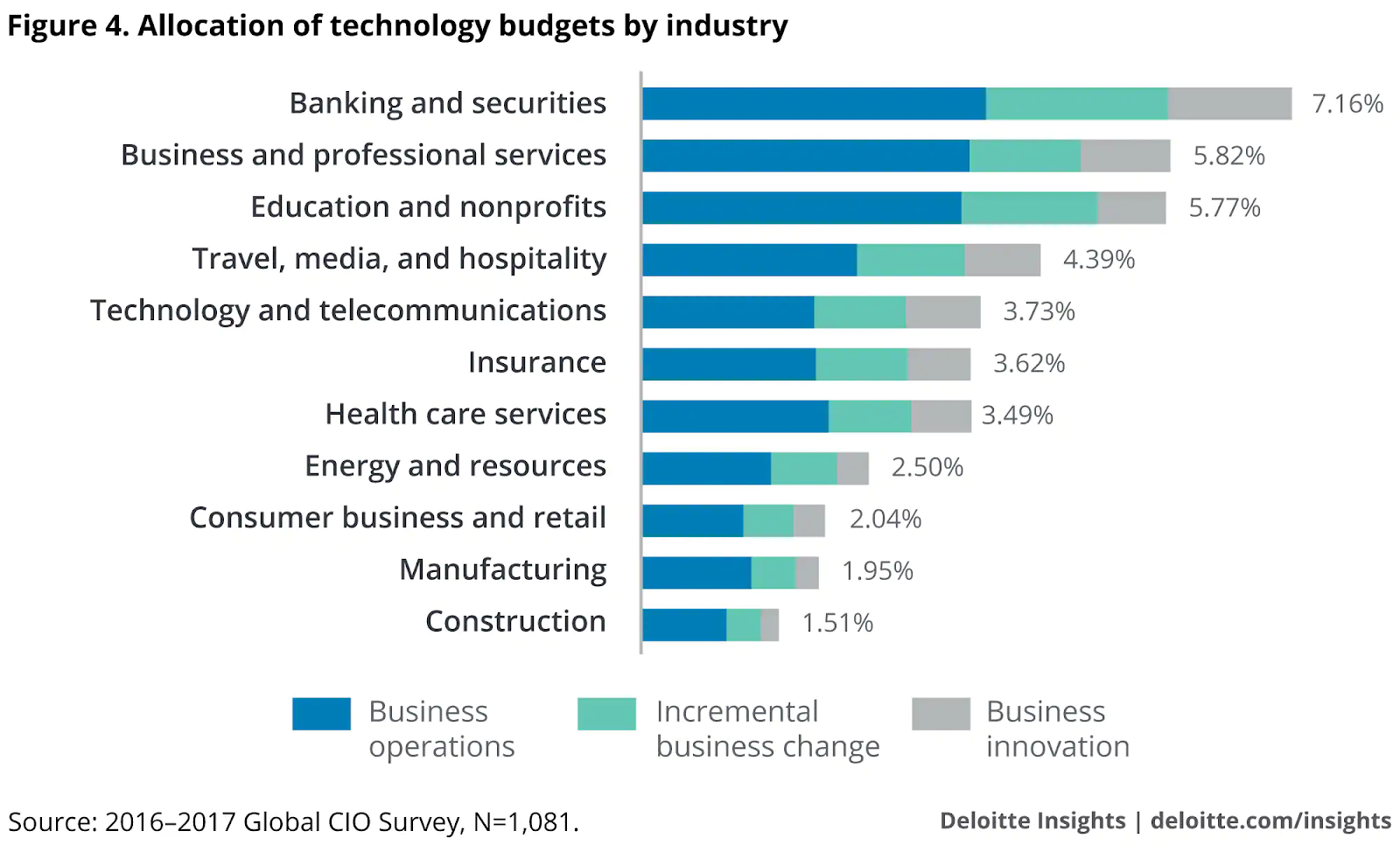

A Deloitte survey found that organizations invested around 0.6 percent of their revenues on digital transformation in 2018. Deloitte assumes IT budgets tend to be set at levels roughly 3.3 percent of revenues.

In principle, digital transformation could therefore account for about 18 percent of IT spending at some companies.

Some might argue that new initiatives overall can represent 15 percent to 40 percent of total IT budgets, the broader transformation initiatives including IoT. The larger figures are likely to be relatively short-lived efforts, though. Over a longer period, most of us likely would be more comfortable with something on the order of 15 percent to 20 percent of all “new initiatives.”

Even if one posits that investment is shifting from maintenance to growth or digital transformation initiatives, how much of that could be spent on IoT is a real question, in any single industry, country or firm.

The issue then is what percentage of digital transformation IoT could represent. At this point in time, the answer would seem to be “not too much,” as few firms have likely moved beyond the “thinking about” or “piloting a solution” phase.

What Percentage of IT Do You Think IoT Represents?

Unless you believe most enterprises operate so effectively that maintenance spending and routine upgrade costs can be capped to prioritize internet of things projects, there are limits to how much most enterprises actually can devote to new IoT initiatives.

In most industries, firm revenue sets boundaries on possible IT spending, since IT spending tends to run at about 3.3 percent of revenue, according to Deloitte. Also, such spending varies widely by vertical. Some manufacturing firms might spend 1.4 percent of revenue, while health care organizations might spend as much as 5.9 percent.

Th

Th

The broad implication is that all IoT forecasts must be evaluated against total IT spending, as no enterprise can actually allocate all of its IT capital and human resources to IoT alone. And that means IoT has to be some fraction of total IT spending, and likely a relatively small fraction, at this point.

IoT Market Size Assumptions are Everything

One problem with estimating the size of the internet of things market is that it is built out of existing parts of existing markets. Semiconductor content, software, appliances and devices, implementation and consulting services already enumerated elsewhere conceivably could also be counted as part of IoT spending.

For that matter, so can the cost of many enterprise information technology projects, when labor costs are allocated.

The bottom line is that all present IoT forecasts, and likely all forecasts for some time, will be subject to huge variations based on assumptions which must be made to separate out IoT spending, now or in five years.

The global IoT market will grow to $457 billion by 2020, at a compound annual growth rate of 28.5 percent, by some estimates, but is quite a bit larger if consumer wearables are included. In that case, current IoT spending exceeds $3 trillion, reaching $9 trillion by perhaps 2020.

Looking only at enterprise markets, and excluding consumer IoT, the enterprise IoT market might reach $6.7 trillion in 2020, if those projections are close to reality.

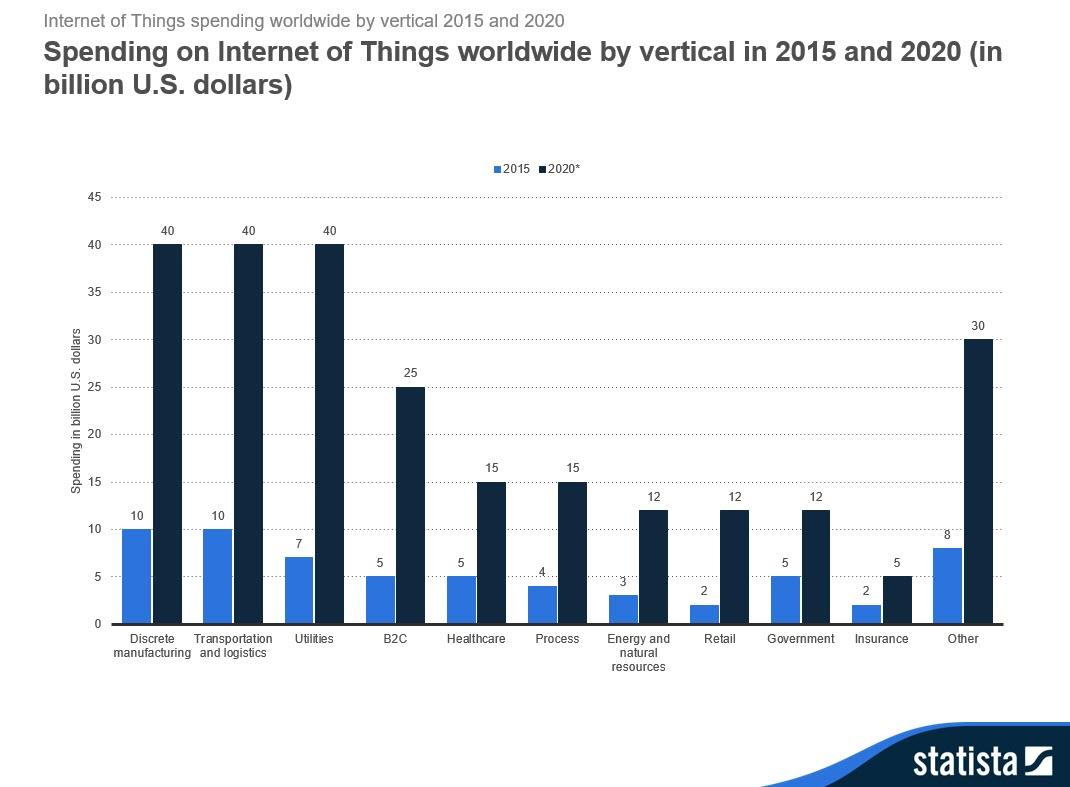

Discrete manufacturing, transportation and logistics and utilities will lead all industries in IoT spending by 2020, averaging $40 billion each, some predict.

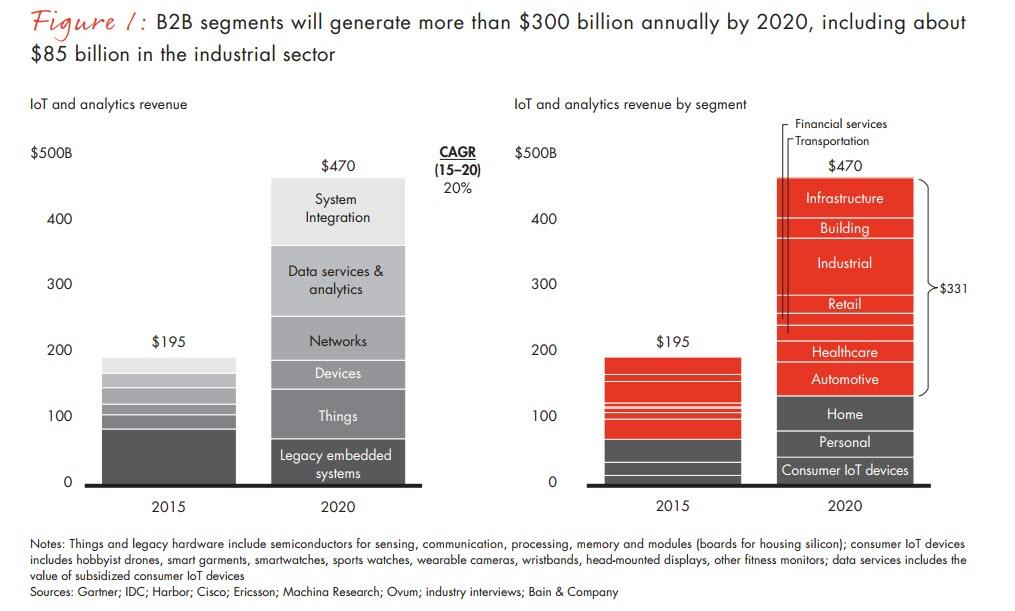

Separately, Bain predicts business-to-business IoT segments will represent $300 billion annually by 2020, including about $85 billion in the industrial sector. For its part, Boston Consulting Group predicts the IoT market will reach $267 billion by 2020.

But by some estimates, IoT endpoints alone might represent nearly $3 trillion in annual sales by 2020, including consumer devices. Looking only at enterprise spending, possibly $1.5 trillion worth of enterprise IoT endpoints might be acquired in 2020.

IoT Endpoint Spending by Category (Millions of Dollars)

Category

|

2016

|

2017

|

2018

|

2020

|

Consumer

|

532,515

|

725,696

|

985,348

|

1,494,466

|

Business: Cross-Industry

|

212,069

|

280,059

|

372,989

|

567,659

|

Business: Vertical-Specific

|

634,921

|

683,817

|

736,543

|

863,662

|

Grand Total

|

1,379,505

|

1,689,572

|

2,094,881

|

2,925,787

|

Right now, our estimates are pretty rough.

Could IoT Already be a $300 Billion to $800 Billion Business?

It is a logical question to wonder how big internet of things markets (hardware, software, services) might be, now or in the future, in any particular industry or country. It is an almost-impossible task, though we must try.

So measure IoT forecasts against global information technology spending, as a reality check.

The key assumption there is that new IoT spending will have to come out of existing budgets that grow perhaps three percent a year, on average.

Global IT might range between $4 trillion and $5 trillion globally. But most believe IoT will happen first in some geographies, including China, the United States, Korea, Japan and Western Europe.

So is $300 billion in enterprise spending on IT (for hardware, software, services) by about 2020 feasible? A good case can be made that this is feasible.

Assume 75 percent of IoT spending therefore happens in China, the United States, Korea, Japan and Western Europe. Assume those countries also represent 75 percent of global enterprise IT spending.

Assume that no more than 10 percent of enterprise IT spending in those areas can be spent on all manner of IoT projects. If global IT spending is $4 trillion. That implies IT spending in the United States, China, Japan, Korea and Western Europe is about $3 trillion. So 10 percent of that amount is about $300 billion.

By some forecasts of IoT by key verticals, 2020 global IoT spending by enterprises could reach about $258 billion.

Global IoT forecasts range from less than $300 billion and up to $500 billion in the enterprise segment.

Some of the bigger figures include the value of consumer wearables and consumer IoT generally, in which case substantially-larger forecasts are made. Add in the consumer use cases and some might estimate present IoT revenue at as much as $800 billion.

According to IDC, worldwide spending on the Internet of Things reached $772.5 billion in 2018, up 15 percent from the $674 billion that was spent on IoT in 2017.

So IoT spending might already be in the range of $300 billion to $800 billion, counting hardware, software, consulting and implementation costs, including the value of staff labor.

But that is not how most researchers tabulate "markets," often the value of hardware, software or other products and services sold in a particular year. By that measure, the IoT market is significantly smaller.

Taking out the allocated portion of enterprise IT labor, and assuming hardware and software, for example, might represent 40 percent of total spending on IoT projects, the "market" for Io

IoT might also be $120 billion. The market for hardware and software might be $320 billion, the higher figure dependent on including consumer appliances including smartwatches and smart speakers and even video appliances in some cases.

Subscribe to:

Posts (Atom)