It has been a couple of decades since we faced systemic risk, major fraud or major overinvestment in what we now call digital infrastructure facilities. Around the turn of the century the issue was overinvestment in data transmission capacity, optical cable networks and local access networks.

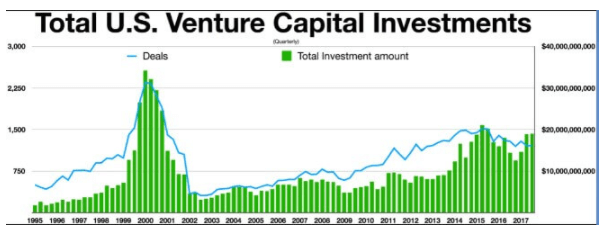

In the five years after the Telecommunications Act of 1996 went into effect, telecommunications companies invested more than $500 billion in capacity, mostly financed with debt. About $2 billion in market value was lost when the investment bubble popped.

Some argue technology startups are once again in a bubble that is bursting. And though venture capital investment is quite different from private equity, some might worry that PE investment in digital infrastructure is overheated as well.

There are micro and macro level risks. At the micro level, some firms might wind up overpaying for assets, overinvesting in assets and then finding themselves insolvent. At the macro level, as often happens, we might see the whole infrastructure market flooded with capacity far beyond demand.

Since nobody is in charge of the whole market, investment booms will tend to overshoot. Eventually, we will have an oversupply of capacity, compared to demand.

It might be easy to argue that investors are rational, and will not again fall prey to excessive enthusiasm. But greed is a powerful motivator. The fear of missing out appears at times to overrule other considerations.

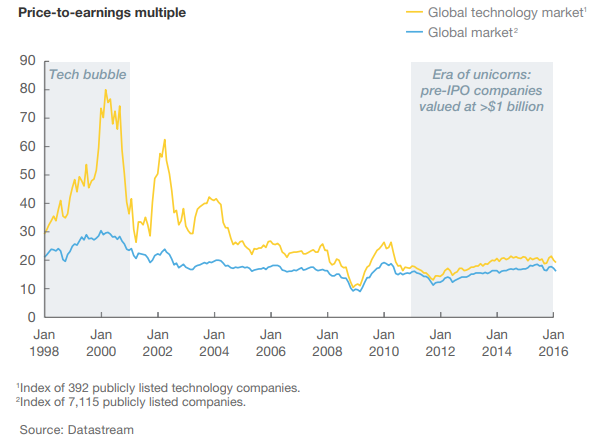

On the other hand, some might note, the current valuation reset for venture-funded technology firms is different from 2000-level valuation in part because most of the present venture-funded firms actually have visible revenue models. The issue is valuation, not a viable revenue model.

There are public market implications as well. After the 2001 internet bubble burst, firm valuations spent roughly a decade resetting to “rational” levels.

Excessive investment between 1995 and 2001 led to a sharp destruction of wealth, although levels of investment had been on an upturn before the exuberance phase.

Again, VC investors operate in a different part of the market from private equity or other institutional investors. The point is simply that enthusiasm sometimes can overtake a segment of the market, leading to overinvestment.

When--and if--that happens in the digital infrastructure market is hard to predict. But some might see increasing levels of threat as valuations climb and low-cost capital availability shrinks. Some later-stage deals might take longer to produce expected profit levels, or produce less profit than originally expected.