Edge computing infrastructure has been among the beneficiaries of investment by both operators (data centers) and investors (private equity and others). But a climate of rising interest rates will not be so helpful for investors, whose payback models have been built on cheap investment capital.

Operators are not driven so much by the level of interest rates, but more by the strategic need to support their customers with edge solutions. The level of interest rates matters, but not so much as for investors.

What we will have to see is the impact on digital infrastructure privatizations in the near term. If interest rates climb to five percent or more, it is going to affect the payback model for taking digital infra (towers, data centers, distribution networks) private.

Low interest rates have meant cheap borrowing costs. All that is going in reverse now, as monetary policy is shifting to higher rates to halt inflation. Higher borrowing costs should slow dealmaking, as payback models get worse.

On the other hand, if inflation remains high there are other risks, including severe recession, which likewise would affect deal flow. On the other hand, severe recessions also create buying opportunities for firms with available capital, able to snap up distressed properties.

So the digital infrastructure investing boom will face new challenges over the next several years, some negative, some perhaps positive. Continued high inflation will mean continued rate increases, a negative. On the other hand, high inflation also can boost asset values, a possible positive.

Stagflation and recession should slow dealmaking while putting pressure on price multiples. Again, some negative and some positive effects will occur.

Still, a clear impact might be that the wave of private equity purchases of formerly public infrastructure from service providers would slow, as interest rates rise.

How much slower is the issue, and for how long. Observers do not expect five-percent (or higher) interest rates for the long term, but activity will hinge on the level of rates and their duration.

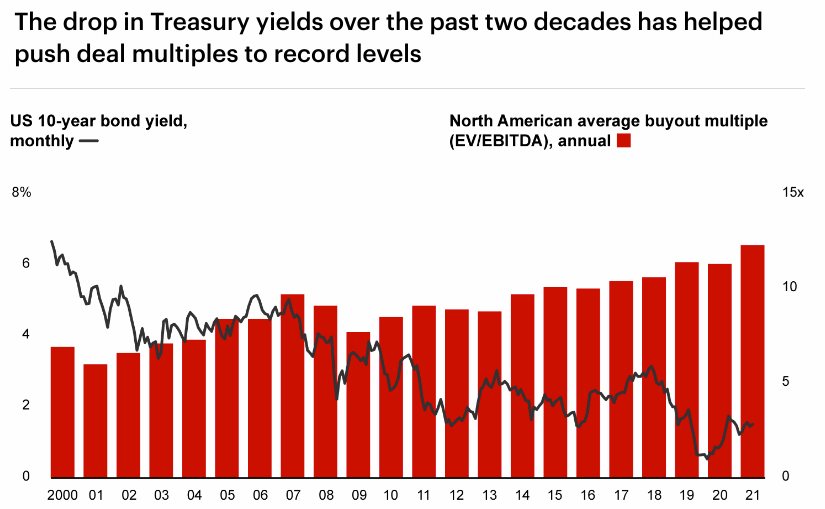

In fact, the whole digital infra privatization business has been fueled by near-zero “real” interest rates. Inflation rates also matter, as they affect “real” interest rates. For the whole class of “alternative” infrastructure (power utilities, roads, airports, oil and gas, renewable energy and data centers, towers and fiber infrastructure), expected returns have been dropping, and specific returns for digital infra might arguably be closer to five percent than 10 percent.

But that is why five-percent interest rates slow activity. If the expected return is five percent, borrowing costs are five percent and inflation rates are high, investments no longer make sense.

The point is that it would not be unexpected to see a slowdown in digital infra privatizations for a while. The business case--with higher interest rates--does get worse.

-----------------------------

No comments:

Post a Comment