Latency performance always is cited as the driver for edge computing and often as the rationale for network slicing.

But even when application requirements are not the issue, transport costs can be.

Latency performance always is cited as the driver for edge computing and often as the rationale for network slicing.

But even when application requirements are not the issue, transport costs can be.

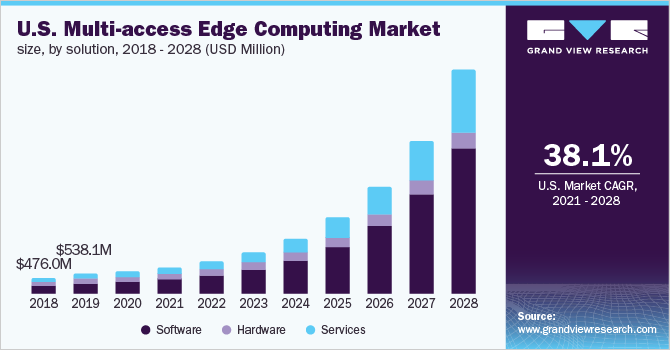

Juniper Research predicts that annual investments by telecommunications operators on multi-access edge computing infrastructure will reach $11.6 billion in 2027, up from $5.4 billion in 2022; a CAGR of 16.7 percent.

By 2027 mobile operators will have built out more than 3.4 million MEC nodes, up from less than one million by the end of 2022.

Juniper forecasts that over 1.6 billion mobile users will have access to services underpinned by MEC nodes by 2027, up from only 390 million in 2022.

Of course, that is a prediction about capital investment, not revenue. And revenue also is a complicated matter where it comes to edge computing. Edge computing spending can represent purchases of user or network devices; software capabilities or computing as a service or 5G access to support edge computing.

So revenue can accrue to a number of participants in the edge computing ecosystem: device retailers, network infrastructure providers, software suppliers or connectivity service providers. So when researchers talk about MEC revenue or investments, one has to separate shares within the ecosystem.

Some estimates have total MEC revenues exceeding $25 billion by perhaps 2027 and close to $70 billion by 2032. Other estimates suggest annual revenue of close to $17 billion by 2027.

But those forecasts virtually always lump together revenues earned by hardware, software and services suppliers: infrastructure and platform plus computing as a service revenues. And computing as a service revenues will likely be dominated by hyperscalers, not mobile operators.

Connectivity providers will profit from real estate support and some increase in connectivity revenues, but relatively rarely from the actual “edge computing as a service” revenues.

For example, assume 2021 MEC revenues of $1.6 billion globally; a cumulative average growth rate of 33 percent per year; services share of 30 percent; telco share of service revenue at 10 percent.

The actual MEC revenue from MEC is quite small by 2028. In fact, too small to measure. Of course, all forecasts are about assumptions.

One can assume higher or lower growth rates; different amounts of connectivity provider participation in the services business; different telco shares of the actual “computing as a service” revenue stream; greater or lesser contributions from mobile connectivity revenue from MEC.

The point is that actual MEC revenues earned by mobile operators or other connectivity providers might actually be quite low. So value earned from all those infrastructure investments would have to come in other ways.

Higher subscription rates; higher profit margins; lower churn; higher average revenue per account are some of the ways MEC could provide a return on invested capital. Some service providers might actually provide the “computing as a service” function as well, in which case MEC revenues could be two to three times higher.

But many observers are likely to be disappointed by the actual direct revenue MEC creates for a connectivity provider.

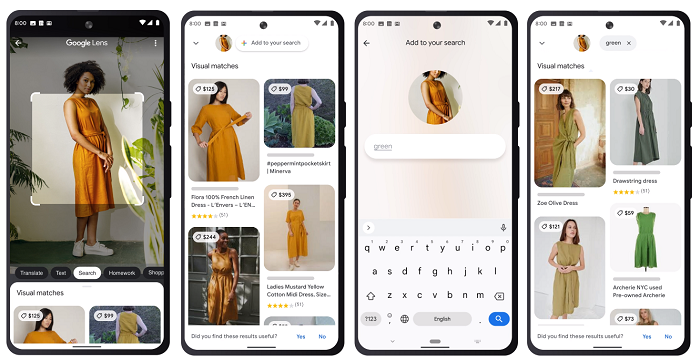

Google’s multisearch function, which will support searching with images and text at the same time. Google likens the experience to pointing at something and asking a friend about it.

That is part of a broader trend: a continuing development of “realism” in media and content. Realism is said to be enhanced by immersion: into a game; a shopping experience; a meeting. So in a broad sense, the many changes that are said to be part of “metaverse” experiences are simply the latest evolution of realism in content and media.

Structured search keeps getting better, and multisearch is just one example of how realism is manifest at a concrete level.

Movement in the direction of greater realism is broadly what the metaverse might be said to represent, though some would likely focus more n “immersion” than “realism.” Realism and immersion are hard to separate.

The objective of high-performance videoconferencing always has been the feeling that “you are there.”

BT says it will use Amazon Web Services as its compute platform supporting internal BT operations. It no longer is a novel move, as many tier-one telcos have concluded it makes sense to use public cloud platforms as they move to cloud native operations.

AT&T shifted non-network functions to Azure back in 2019. Deutsche Telekom, Vodafone and Verizon have moved apps to public cloud providers. Telefonica, SKT, Singtel, Optus and Globe Telecom are among service providers moving workloads to the public cloud.

In principle, telcos, no less than any other large enterprise users, simply are shifting with the larger changes in computing architecture towards remote computing and content access.

Such deals have been cited as possibly problematic in some quarters, with the issues viewed as increasing vendor lock in.

The issue is not so much the exporting of the computing platform but the difficulty of switching cloud computing suppliers in the future, should that be desirable.

That is valid, but no more so than would be the case when other major compute platform choices are made.

A survey conducted for Google Cloud by Omdia suggests North and South American; Asia and European enterprises and mid-market firms are planning on using at least one 5G or other edge computing element within the next year.

Though we are accustomed to suppliers issuing such forecasts (“demand for our product is skyrocketing”), in another sense it would be odd indeed if virtually any business was not already using some form of edge computing (local processors), or planning on adopting 5G to some extent.

Edge computing is what a PC, smartphone, tablet or a router does, for example. By definition, a 5G smartphone does some amount of edge computing on the device.

Of course, that is not what Omdia and Google Cloud were looking to explore. Instead, they were looking at a shift of business computing from some on-premise mode to remote computing at the edge. And buying of edge computing services and infrastructure is planned by close to 70 percent of survey respondents.

Some use cases already are common among edge computing adopters. Video and other data analytics, as well as storage, are key use cases.

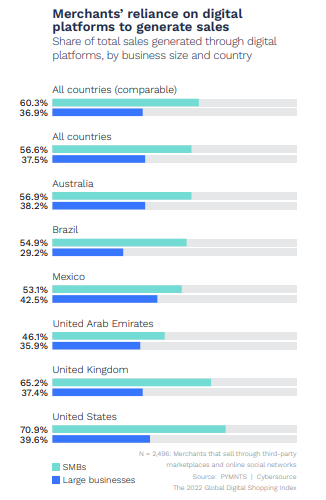

In some ways, small businesses are “more digital” than enterprises where it comes to sales tools, a survey conducted by Payments.com suggests.

“The average SMB now offers a 24 percent more frictionless shopping experience than larger competitors,” Payments.com says. “This is largely because SMBs provide far more digital and cross-channel shopping features than larger businesses.”

“SMBs are 46 percent more likely than larger businesses to offer cross-channel-capable digital profiles, for example, and 44 percent more likely to allow shoppers to pick up e-commerce orders at in-store kiosks,” Payments.com says.

One suspects there is a bit of unavoidable structural bias, though. Many enterprises do not sell direct to end users, so there is no requirement for direct-to-consumer sales platforms.

During the recent Covid pandemic, many small businesses were forced to sell in non-traditional ways, as customers were prevented from entering their stores.

SMBs in Australia, Brazil, the U.K. and the U.S. the four countries Payments.com studied in 2020 and 2021, adopted 13 new shopping features between 2020 and 2021. All can be categorized as aid five aspects of the buying experience:

Know me

Value me

Know what I want

Make it easy

Protect me

In nearly every country, the seven most common features SMBs added included voice enabled purchasing, buy online, pickup in-store options, price matching, digital profile support, mobile apps allowing consumers to locate items in physical stores, payment information sharing and coupons consumers could access across purchasing channels.

SOURCE: Payments.com