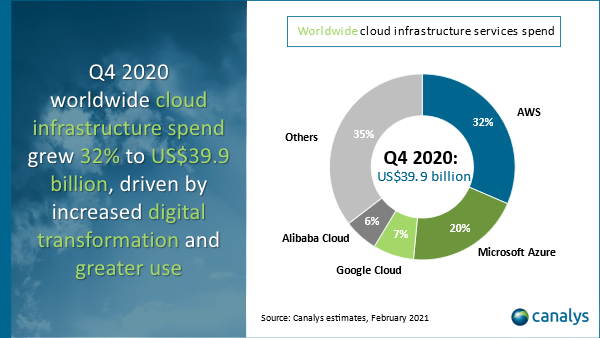

Cloud computing, as with most other markets, has a small group of market share leaders: Amazon Web Services, Microsoft, Google and Alibaba.

source: Canalys

Stil, it never is easy to compare installed base or market share when suppliers count revenue and sales in different ways. That is a clear issue for cloud computing as a service. Microsoft’s installed base is inflated, when compared to other suppliers.

Azure revenue includes sales of the Windows operating system, productivity suites, Xbox, Surface and advertising. Also, keep in mind that Azure cloud computing also includes server sales, not just “cloud computing as a service” revenues.

The “intelligent cloud” segment of Azure represents only about 35 percent of total Azure revenue. Another third of Azure revenue comes from productivity suite revenues. Also, 32 percent of Azure revenue comes from operating systems, productivity suites, Xbox, Surface and advertising.

I personally do not consider those revenue sources a “like to like” comparison with AWS cloud computing as a service revenues. Actual Azure cloud computing revenue. might be as low as $4 billion a quarter. The point is that any analysis of cloud computing market share based on Azure revenue is incorrect.

Azure cloud computing might be only a bit larger than Google Cloud, which generated about $3.4 billion quarterly revenues recently.

source: Canalys

China spending on cloud services grew 55 percent in the first quarter of 2021, says Canalys, increasing spending 2.1 billion (€1.77 billion) over first quarter of 2020 levels and up $200 million (€168.13 million) sequentially.