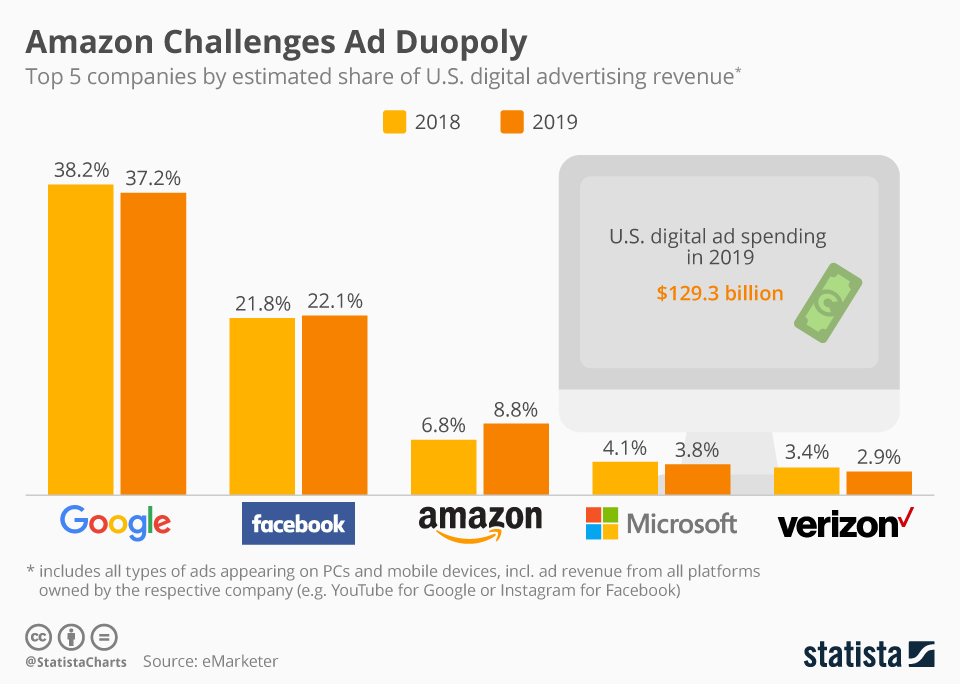

When one thinks about online advertising, most of us would guess Google and Facebook are dominant in the field. We tend not to think of Amazon as a significant and fast-growing participant. Verizon and AT&T have smallish positions right now, but AT&T expects to become a bigger player as it harnesses its Warner Media content operations and assets.

Similarly, when thinking about edge computing, the names Amazon and Verizon, along with a few other tier-one connectivity providers--including Vodafone, KDDI and SKT--have recently popped up. Amazon notably will provide its Wavelengths edge computing service, while the telcos supply edge computing real estate.

But other perhaps unexpected names will emerge. Already, Walmart, the giant U.S. retailer, now says it will build edge computing facilities available to third parties. Developments such as that show the challenges telcos will face in securing a role in edge computing. On the other hand, such hyper competition is not unique. Most big markets are susceptible to disruption.

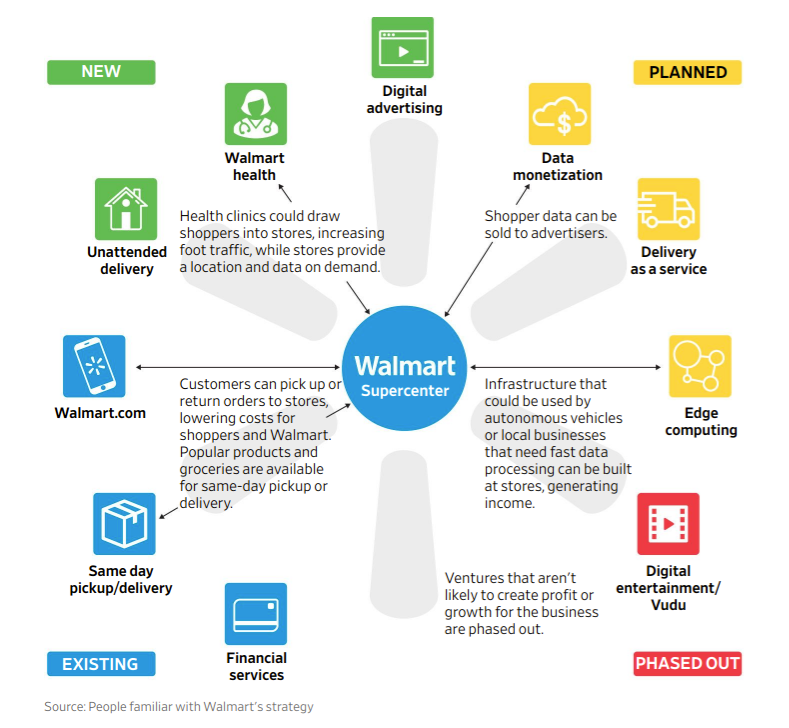

For example, Walmart believes it must take a greater share of advertising, in part to sustain profitability of its online commerce operations.

Much as Amazon can pitch itself as a valuable ad venue because it knows what products people are searching for, right now, so Walmart hopes its shopper data can make it a place for advertising about related products after actual purchases have been made, for example.

The point is that Walmart might well be competing in a number of businesses we might not have expected. As it plans to make its edge computing services available to third parties, so Walmart now expects its own logistics capabilities to be offered to third parties.

Much hinges on how extensive an edge computing network must be, in a metro area, to support many classes of new applications requiring low latency. If, as many telco execs now believe, only one major metro edge computing site is required, competitive entry is easier for any number of new players.

If dispersed edge computing sites, with even lower latency are required for some use cases, then competitive entry is more difficult. It simply is not clear yet how extensive edge computing sites must be to support autonomous vehicles, for example.

Many observers would note that telcos often have stumbled trying to enter new fields where other providers--incumbent and upstarts--also have aspirations. It already looks like competitors in the edge computing market are moving fast, which could limit the revenue upside for telcos in the broader edge computing business.

No comments:

Post a Comment