Some markets are more complicated than others. Internet of things, which might not even be a single market, is really complicated.

Also, we sometimes see forecasts for functions that are part of markets. Consider network slicing, which some now see as a discrete market. But network slicing can be seen as a function produced by a virtualized network, which itself is function of core networks. So is the market network slicing, virtualization or capital and other spending on next-generation networks?

The decisions matter since overcounting is the danger (counting a unit of revenue multiple times, for example).

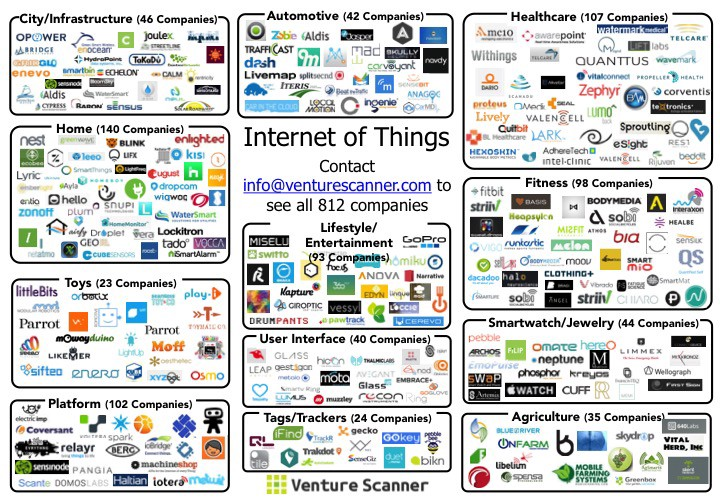

Consider this visualization of consumer wearable, smart city, precision agriculture, smart home, healthcare, automotive, logistics and a few platform segments as well.

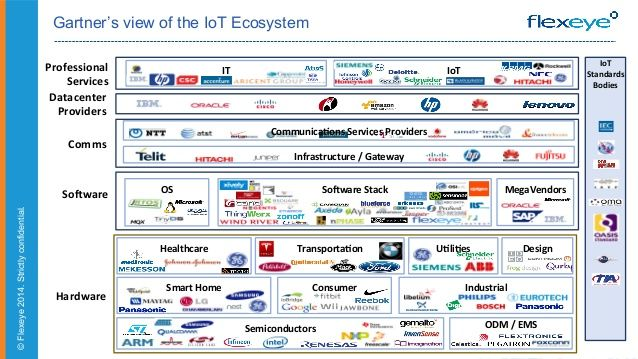

Other more horizontal approaches are superficially less complex, but only superficially.

Consider the automotive IoT marketplace, which is robustly complex, as are other vertical markets, featuring perhaps hundreds of direct participants.

So imagine the plight of any business professional trying to make sense of the opportunities. Revenue forecasts given the participation by thousands of potential companies, quickly can be ridiculously--and most likely falsely--large. For the IoT market is not the simple sum total of revenue earned by all firms who claim to be in the business.

IoT revenue is the incremental amount of new activity that does not displace existing spending on underlying functions (hardware, software, consulting, integration and so forth).

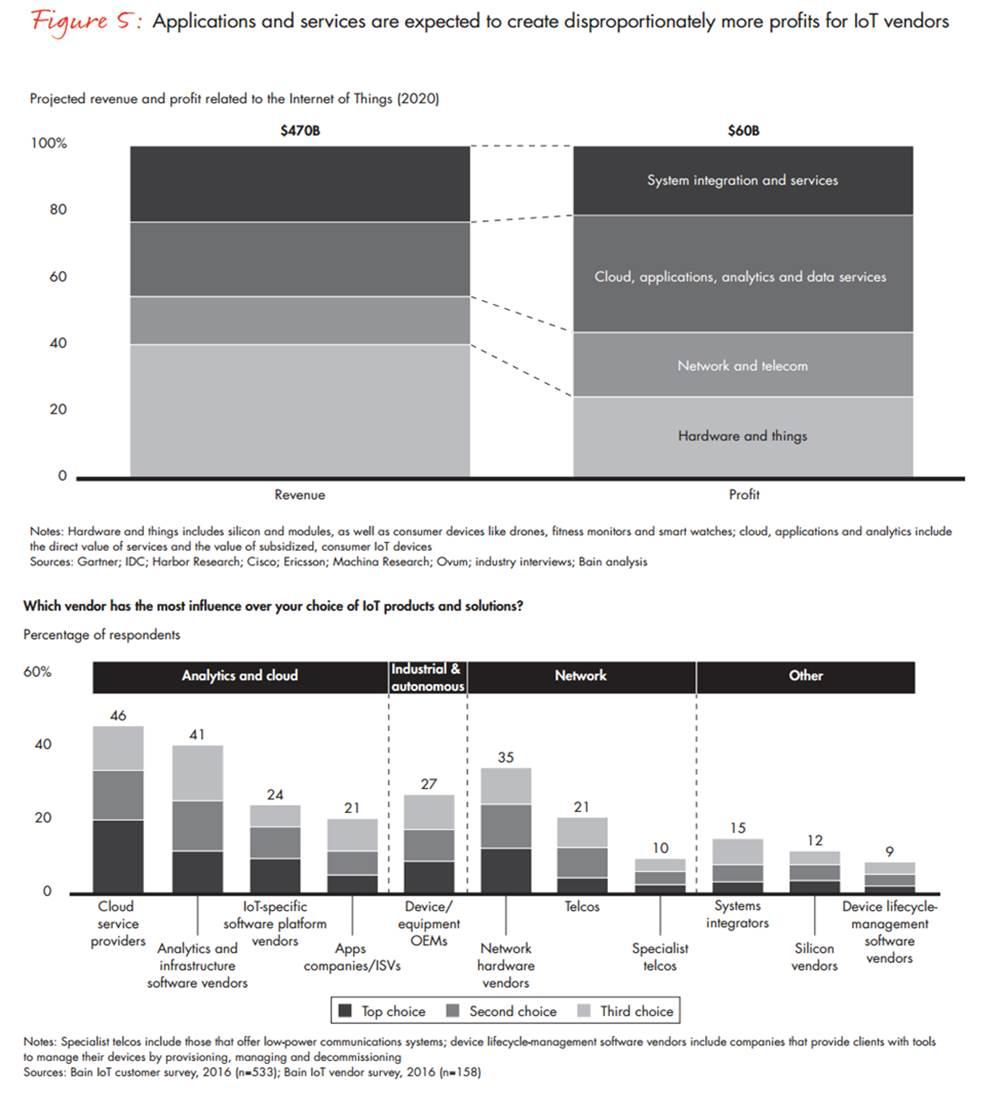

So could IoT generate revenue as large as $3 trillion by 2025? Here are a few assumptions made by Machina Research in creating the forecast. The researchers assume about $1.3 trillion in direct spending on hardware, software and services, with the balance of revenue located upstream or downstream in the ecosystem.

Chipsets would be downstream, while the rest of the revenue is earned in other ways. That notion seems to be built around the idea of economic impact. Perhaps, as McKinsey analysts argue, there is the attributable value of cloud computing more generally, advanced robotics and so forth.

That is not to say broad economic impact is an invalid concept. But economic impact studies normally rely on multiplier effects to generate a sense of ecosystem benefits. That is something quite different, and quite a bit bigger, than direct sales of products and services in any single industry. And that is where most of the big numbers related to IoT forecasts are found.

The other issue is that, by many accounts, as much as 40 percent of total IoT spending could be for devices and “things” (including smart watches, often smart TVs and other appliances, connected cars and so forth). So right off, some of us would tend to discount the value of the connected appliances, and perhaps only include the value of sensors, for example.

That is not to say a smartwatch or connected security system or vehicle is not, in some way, part of the IoT ecosystem; only to note that for analytical purposes such purchases also are normally counted as part of some other value chain.

IoT markets are nearly impossible to quantify with any precision because there simply are too many moving parts right now.

No comments:

Post a Comment