"A stable competitive market never has more than three significant competitors, the largest of which has no more than four times the market share of the smallest,” Bruce Henderson, founder of the Boston Consulting Group has argued.

Sometimes known as “the rule of three,” he argued that stable and competitive industries will have no more than three significant competitors, with market share ratios around 4:2:1.

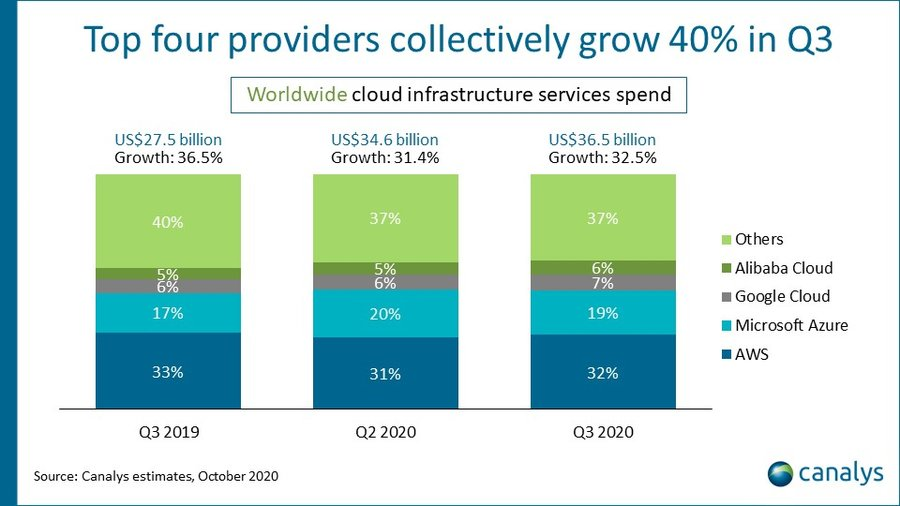

If you look at market share in the “cloud computing as a service” industry, one does not yet see that pattern, suggesting major market share shifts are likely. But most of the activity, all other things being equal, will happen at positions two to four.

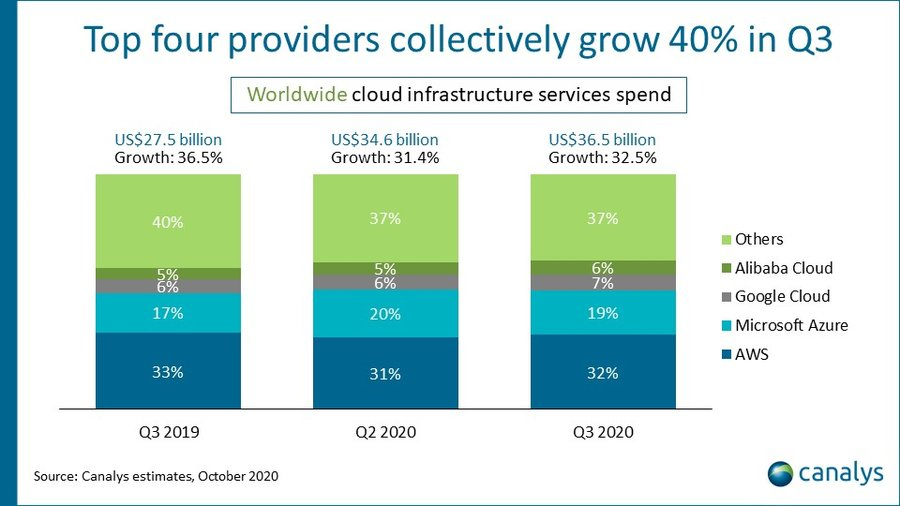

AWS now has 32 percent share. By some estimates Microsoft has 19 percent share. Google Cloud about seven percent share. The rule of three would predict either that AWS eventually would have more share, or that number two would have less share, or both.

I believe the reported numbers overstate Microsoft’s share and understate Google’s share, however.

source: Canalys

If a “like to like” analysis of “computing as a service” revenues are made, Microsoft’s actual cloud revenues are far smaller than reported.

The problem is that the way Microsoft reports revenue dramatically skews the results.

Azure, which includes cloud computing revenue, also includes sales of the Windows operating system, productivity suites, Xbox, Surface and advertising.

Also, keep in mind that Azure cloud computing also includes server sales, not just “cloud computing as a service” revenues.

The “intelligent cloud” segment of Azure represents only about 35 percent of total Azure revenue. Another third of Azure revenue comes from productivity suite revenues. Also, 32 percent of Azure revenue comes from operating systems, productivity suites, Xbox, Surface and advertising.

I personally do not consider those revenue sources a “like to like” comparison with AWS cloud computing as a service revenues. Actual Azure cloud computing revenue. might be as low as $4 billion a quarter. The point is that any analysis of cloud computing market share based on Azure revenue is incorrect.

Azure cloud computing might be only a bit larger than Google Cloud, which generated about $3.4 billion quarterly revenues recently.

If so, AWS market share is understated and Microsoft’s share is vastly overstated. At $4 billion quarterly revenue, Microsoft likely has about 11 percent share. Google might have about nine percent share.

If AWS generated about $11.6 billion in revenue in the third quarter of 2020, then AWS did have about 32 percent of global cloud computing market share.

A corollary is that, all things being equal, it will be very hard to supplant Amazon Web Services as the market leader. It is unclear at this point which firm emerges as a stronger number-two provider. Many seem to be betting on Microsoft, based on its apparent or reported growth rate.

In the absence of better data, it is hard to say.